Fertilizer Sector: 4Q22 Earnings Overview

Fertilizer Sector: 4Q22 Earnings Overview

Earnings season is over. Let's dig into it

4Q22 at a glance

The quarter came out mixed: fertilizer prices moderated after peaks of 1Q-2Q22, but remained high compared to the historical levels, demand was destroyed, and farmers stepped back from the market. Thus, companies were sold at good prices, but in much smaller volumes.

At the same time, inflationary pressure was building. Add to this high base of 4Q21, and we get that ~50% of companies reported a YoY decline in their EBITDA. In absolute terms, the numbers remained strong, but it’s clear that the peak has been passed and the days of growth are over.

These figures themselves are not so important, as the market has changed significantly since then - demand weakened further, fertilizer prices fell 20-40%.

What’s interesting is what companies tell us about current conditions and what they expect.

What management says about 2023

I listened to many conference calls that accompanied earnings releases (highly recommended if you have a sleep problems). In general, management comments were the same:

They note weak demand in Jan-Feb ‘23. Fertilizer prices fall against the backdrop of a weak demand, and farmers are in no hurry to return to the market - why to buy now if you can buy later cheaper?

Things are to change soon. After a mute 1Q23, companies expect demand to catch up during the planting season in the Northern Hemisphere. This should be supported by improved farmers economics (high crop prices, cheaper fertilizers).

They expect nitrogen prices to bounce with recovering demand. Prospects for potash are muted - many don’t believe in growth from current levels.

Those who gave guidance, expect 2023 EBITDA to fall 25-40% YoY.

There are no capex-intensive projects in their pipelines, they plan to distribute 2023 free cash flow among shareholders.

Market reaction

The market was not excited, stocks were first down on earnings miss, then up. As a result, we are now where we were a month ago.

My view

Always take management comments with a grain of salt. I remind that they discussed recovering demand for fertilizers during previous earnings calls (in Nov-22). And it didn’t happen back then.

Also, don’t underestimate the weakness of 1Q23. Since companies' realized prices are usually spot with 1-mo lag, we can expect 1Q23 prices to be down 20-30% YoY, which will mean significantly smaller profits compared to 1Q22.

However, I agree with some theses and believe that we are near the bottom (mainly in urea):

Application season is around the corner (this time for sure), farmers and retailers will need to step back into the market to get their products.

Fertilizers affordability (ratio of crop prices to fertilizer prices) is indeed better, than it was in 2022.

Domestic urea prices in China are now above the international prices ($400/mt vs. $360-380/mt), so it could export less favoring attractive domestic market. This should tighten the global supply and increase international prices.

Another barrier for further decline in urea prices is domestic prices in Russia at $350/mt. If international prices fall below this level, we may lose another chunk of global supply, as Russian producers will try to sell domestically instead.

Last week, urea prices jumped on expectation of the Indian purchase tender, but didn't plunge back after it was revealed that the tender terms are quite disappointing - I think this confirms that the market is tightening ahead of spring demand.

However, I’m puzzled by the magnitude of a possible rebound in prices. Over the last several months, we’ve seen that high prices destroy demand. So large rebound is unlikely, imo.

Below are highlights from the results and calls.

Nitrogen

CF Industries (NYSE: CF)

Plants location: US. Main products: urea, UAN, ammonia

Call takeaways:

Company notes demand destruction and weak prices in Jan-Feb ‘23. Thinks that this will change in 2Q23 with the spring demand.

Over the last two weeks, it has seen some retailers trying to step back into the market, as prices became attractive.

Expects that additional corn and wheat acres in the US will drive demand for additional 0.3-0.4mmt of fertilizers in 2023.

Expects that there will be plenty of cash for both green investments and shareholders return. Sees 2023 capex at $500-550mn vs. $450mn in 2022 and $500mn in 2021.

CVR Partners (NYSE: UAN)

Plants location: US. Main products: UAN

Call takeaways:

Plans no turnarounds at its facilities until the fall 2024, which means stronger production this year.

Expects that spring demand will be strong due to improvement in fertilizers affordability.

Thinks that high European gas prices will continue to affect global fertilizer prices through 2023.

LSB Industries (NYSE: LXU)

Plants location: US. Main products: UAN, ammonia

Call takeaways:

Expects that spring demand will be strong due to improvement in fertilizers affordability. Demand should kick in within the next couple of weeks.

Thinks that urea prices will move up faster than UAN and ammonia.

Will not benefit from low US gas prices at ~$3/mmbtu in 1Q23, as it’s locked at $6/mmbtu.

Guides 1Q23 EBITDA at $55-65mn, a 40% YoY decline.

Thinks that there is a high probability that it will be granted with a $100mn from USDA in its Fertilizer Product Expansion Program.

Yara (EURONEXT: YAR)

Plants location: Europe. Main products: urea, nitrates, NPK

Call takeaways:

Its nitrate and NPK products currently enjoy strong premiums to commoditised urea. That helped it to post strong results.

While 35% of its ammonia production in Europe is offline, it has flexibility in sourcing ammonia from other regions.

Says that current ammonia utilization rate in Europe increased to 70% as gas prices moderated.

Expects demand to catch up in most regions.

2023 capex will be at $1.7bn, exceeding usual $1.2bn annual guidance.

OCI (EURONEXT: OCI)

Plants location: Europe, Middle East, US. Main products: urea, ammonia

Call takeaways:

Expects demand catch up in urea and UAN in the US in March.

Thinks that India will need to replenish fertilizer stocks in 2023.

Notes that Russian urea and UAN exports were at record levels in 2022, which means that there is no supply shortage from this side.

Reiterates its strategy focus on development of blue and green ammonia.

Considers buyback given the recent stock price decline.

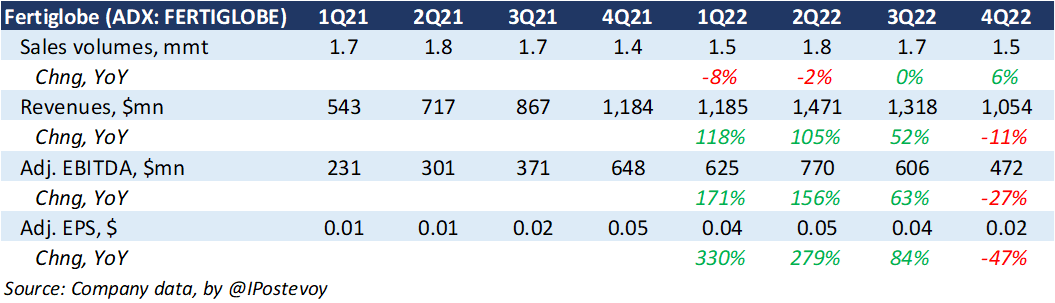

Fertiglobe (ADX: FERTIGLOBE)

Plants location: Middle East. Main products: urea, ammonia

50% owned by OCI. Same management - same comments

SABIC Agri-Nutrients (TADAWUL: 2020)

Plants location: Saudi Arabia. Main products: urea, ammonia

No earnings call

Phosphates, Potash

Mosaic (NYSE: MOS)

Plants location: US. Main products: DAP/MAP, MOP

Call takeaways:

Notes strong ag fundamentals and expects strong catch up in demand (I’m a bit tired of writing the same line for all companies).

Thinks that the recent potash prices decline was due to aggressive marketing of products from Russia and Belarus over the slow winter season.

Sounds very bullish on potash - says that there was a year of low potash usage and soil levels are depleted, so farmers will need to add it to the soil to ensure reasonable yields this year.

Sees that Brazil inventories have worked their way down to much more normalized levels for both potash and phosphates.

Despite its positive expectations, it guides 1Q23 potash sales prices below $500/mt, more than 15% QoQ decline.

In phosphates, it sees tight market, as China shuts down production for environmental reasons. Also, a significant portion of phosphoric acid is now being directed to industrial uses, including the battery market, which reduces supply available for fertilizer production.

Sees 2023 capex at $1.3-1.4bn vs. $1.2bn in 2022.

Maaden (TADAWUL: 1211)

Plants location: Saudi Arabia. Main products: DAP, ammonia, alumina, gold

Call takeaways:

4Q22 EBITDA was affected by some large “adjustments” in aluminum segment. Fertilizer segment, which accounts for 83% of total EBITDA, posted a 17% YoY growth.

Notes strong ag fundamentals in 2023.

In August, it commissioned Ammonia III plant with 1.1mmt ammonia capacity. Development of Phosphate III project is on track (will add 1.5mmt P-ferts capacity in 2025, and another 1.5mmt in 2027).

Focuses on reducing outstanding debt, no set cash dividends at this time.

Guides 2023 DAP production at 4.9-5.6mmt (vs. 5.2mmt in 2022), ammonia at 3.1-3.5mmt (3.2mmt in 2022).

Nutrien (NYSE: NTR)

Plants location: Canada. Main products: MOP, urea, ammonia, UAN

Call takeaways:

Expects demand to come soon, plans to deliver strong earnings across all segments in 2023.

In North America, it sees retail potash inventories being down 15-20% YoY. In Brazil - elevated but normalizing inventories, in India - tight, in China - close to average.

Continues to talk about global potash shortage as a result of Belarus and Russia having reduced export.

Guides 2023 potash sales volumes at 13.8 - 14.6mmt vs. 12.5mmt in 2022. Expects to reach 18mmt of annual operating capability in 2026.

Retail department sees 40% of soil tests in the US being below adequate levels in potash.

Guides 2023 EBITDA at $8.4-10.0bn, 20-30% YoY decline. Assumes that nitrogen prices will strengthen during spring.

Refused to comment on potash prices in 2023 but it looks like its guidance implies average realized price at $430/mt vs. $630/mt in 2022.

ICL Group (NYSE: ICL)

Plants location: Israel. Main products: MOP, DAP/MAP

Call takeaways:

Notes strong demand in Brazil - company is sold out on potash for 1Q23, on phosphates for 1Q and 2Q23.

Guides 2023 EBITDA at $2.2-2.4bn, a 43% YoY decline. Assumes average realized potash prices below $500/mt vs. $682/mt in 2022 and $356/mt in 2021.

Increases focus on Specialty business (food, battery, paints, pharma, building), wants to reduce exposure on commodities.

Thinks that China has healthy potash inventories.

Company’s industrial business was affected by low demand, e.g. in housing. It expects rebound once interest rates to start falling down.

Note: The calls took place during the 3rd and 4th weeks of February. Keep it in mind when you read comments related to timing. Also, these takeaways are a paraphrase and may not be accurate.

Disclaimer: not an investment advice. Always do your own research